- 10 Lenders Said No. SmartLend Found the One Who Said Yes — in 3 Days.

- Singapore SME Grants 2023–2026: What Actually Changed (And What Nobody Tells You)

- Why SME Loan Approval Rates Dropped to 70% — And What the Iran War Means for 2026

- Real CBS Makeovers: 3 Case Studies of SME Owners Who Turned Bad Credit Around

- Ask SmartLend: Why Did My SME Loan Get Rejected?

- Introducing SmartLend Concierge: A Helping Hand for SME Loans

- Legal Ways to Lighten Your Company’s Tax Burden in Singapore

- A Wake-Up Call on Director Duties: The Envy Saga and Other Cautionary Tales in Singapore

- Surviving Cash Flow Crunch: How SMEs Can Use Short-Term Financing Wisely

- Unmasking Business Loan Fraud: How Syndicates and Rogue Brokers Game Singapore’s Lending System—and How AI Can Stop Them

Everything You Need To Know About Writing and Issuing Cheques In Singapore

There is no denying that cheques have become less prevalent as a form of payment today. It

has been reported that 40% of worldwide transactions were made by cheques back in 2005. This number fell drastically to only 16% by 2010, and then to 8% by 2014. Today, cheques have almost completely disappeared in many developed countries such as Germany, the Netherlands, and the Scandinavian nations.

In Singapore, while 40% of all payments were still made through cash or cheques in 2018, the Government has made a fervent push for the adoption of online payment systems and aims for Singapore to become cheque-free by 2025.

Nonetheless, cheques have been in usage for centuries and modern iterations of them have been supported by fairly sophisticated banking systems and bodies of law. So, despite its star being on the wane, there is still merit in knowing how cheques work (particularly for the younger towkays out there who might have less experience with them).

What is a cheque?

A cheque is a paper document that orders a bank to pay a specific amount of money from the account of a person or entity to another person or entity whose name the cheque has been issued in.

Cheques are generally valid for 6 months from the date written on the cheque unless a shorter period is otherwise stated on the cheque itself.

Cheque clearing

Since 2003, all banks in Singapore have implemented an online image-based cheque clearing system known as the Cheque Truncation System (CTS).

How CTS works is that when you deposit a cheque into your account, this cheque is scanned and the electronic image is sent to the payer’s bank for crediting instead of the physical cheque itself. This cuts down the time it takes to credit a cheque amount into an account.

With this system in place, the cheque clearing schedule currently looks like this

Cheque deposited on | Funds available |

Monday to Thursday (before cut-off time) | The following business day (after 2pm) |

Thursday (before cu-toff time) | Friday (after 2pm) |

Thursday (after cut-off time) | Monday (after 2pm) |

Friday (before cut-off time) | Monday (after 2pm) |

Friday (after cut-off time) | Tuesday (after 2pm) |

Saturday | Tuesday (after 2pm) |

A 5-Day Clearing Week means that cheques are cleared from Mondays to Fridays only. Cheque deposit cut-off time is usually at 3.30pm.

Cheques deposited on Saturdays and Sundays will only be sent for cheque clearing on Mondays (or the next business day if Monday is a holiday). This means the funds will only be available on Tuesday.

However, cash cheques can be encashed at the payer’s bank straightaway, even on Saturdays (if the bank has branch banking on Saturdays). A handling fee will be charged for this.

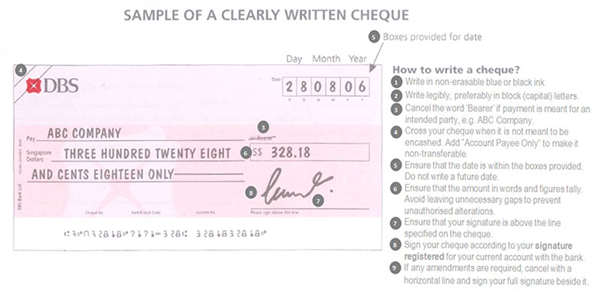

Writing a cheque

There are quite a few things to take note of when writing a cheque to ensure that it can be cashed in without any issues. Below is a sample of what a clearly written cheque would look like:

Credit: POSB

Make sure you have enough money

If there are insufficient funds in the payer's account, the cheque will “bounce”. In other words, it will be rejected. Charges will then be imposed for the return of the cheque as well as the overdraft interest to cover the bank’s loss in overnight interest. More on this later.

Crossing your cheque

For a payee only (non-transferable) cheque:

- Cross the cheque by drawing two parallel lines across the top left-hand corner of the cheque.

- Cancel “or bearer” on the cheque and add “Account Payee Only” (or “A/C Payee Only”).

Both steps must be done in order to prevent this cheque from being able to be deposited into someone else's bank account.

For a cash cheque, there is no need to cross it or to make any amendments to it since the whole purpose of the cash cheque is to disburse the stated amount to the bearer, whoever it may be.

Write the correct amount

- Write the amount in words and write “only” after that.

- Make sure the amount in figures that is written in the box matches the written amount.

- The decimal point must be clearly seen. Do not use a backslash (/) in place of the decimal point as it can be misread as a “1”.

- Use commas to make the numbers look neater and easier to distinguish when writing large amounts. For eg. $1,000,000.

Limit Alterations

Check all details carefully before signing a cheque. If an alteration needs to be made, it can be done if a full signature by the payer is then beside the alteration. However, consider issuing a new cheque instead if there are multiple alterations needed as this can make the cheque look messy and confusing.

How to stop a cheque payment

Payment of an issued cheque can only be stopped if it has not been cleared or cashed out, so time will be of the essence. If you wish to stop a cheque payment, you must get in touch with your bank immediately. An administrative fee will most likely be charged.

What happens if a cheque is returned unpaid (bounced)?

Under CTS, when a deposited cheque is returned unpaid, an Image Return Document (IRD) will be issued to the payee instead of the cheque itself. The IRD serves as a notice of dishonour and legally replaces the original cheque for the purpose of re-presentment for clearing under CTS. This means that in trying to get the bank to cash the original cheque once more, the IRD will be the document to present to the bank, unless otherwise stated.

This presents more convenience for the payee than having to ask for a new cheque from the payer. Should a cheque bounce, simply get the payer to top-up the required amount into the account, and the payee can now present to the IRD to the bank for clearing once more.

Here is a specimen IRD showing the features to look out for.

For the payer, a bounced cheque will result in a handling or administrative fee for the return of the cheque and overdraft (OD) interest charges to cover the bank’s loss in overnight interest.

The original cheque will have been removed from the bank’s clearing process once it has been scanned, so the IRD will most likely be the only prevailing document. If one wishes to retrieve the original cheque for any legal reasons, the bank may attempt to do so if it has yet to be disposed of. However, a retrieval charge of $50 will be applied.

Is issuing a bounced cheque illegal in Singapore?

A cheque is considered a Bill of Exchange. In Singapore, under the Bills of Exchange Act, there is no criminal liability imposed for issuing a dishonoured cheque; only civil liabilities prevail. Damages would frequently include the amount of the cheque, interest from the time of presentment of payment and expenses of noting.

There may be exceptional circumstances, such as when fraud can be conclusively proven (but that would require a far more extensive legal claim than simply a bounced cheque), where criminal liability could be applicable, but those instances are rare.

This may be in sharp contrast to many other countries, even those under a common law system like us - such as India – who do make it a criminal offence. However, Singapore is famously business-friendly. In fact, our Courts have even decided that claims premised on dishonoured cheques are within the scope of arbitration, meaning they would rather the contracting parties reach a resolution by themselves rather than through court proceedings.

What should a payee do if a cheque keeps bouncing?

The Singapore Courts are hoping that for the sake of business relations, contracting parties should treat each other in good faith and not necessarily assume a dishonoured cheque must be a malicious or dishonest act. However, should a cheque remain consistently unable to be cashed and payment is not forthcoming, then the payee will need to take legal recourse.

If the amount is not above S$10,000, the best course of action would probably be to bring a claim before the Small Claims Tribunal. Anything above that would unfortunately require more expert legal advice, even if arbitration is invoked as an alternative resolution.

Read also: How can Singapore Businesses Keep Their Heads Above Water in a Recession

Read also: Things to Take Note When Setting Up A Company in Singapore

Read also: The Best Business Banking Accounts in Singapore

-------------------------------------------------------------------------------------------------------

Not sure whether your company can be qualified for bank loans or alternative lending? Try our A.I assisted loan, and Smart Towkay team will send you a lending report within 24 hours' time. With the lending report, we aggregate and recommend the highest chance of approval be it with BANKS / FINANCIAL INSTITUTIONS or Alternative lenders like Peer to Peer Lenders or even B2B lender!

Got a Question?

WhatsApp Us, Our Friendly Team will get back to you asap :)

Share with us your thoughts by leaving a comment below!

Stay updated with the latest business news and help one another become Smarter Towkays. Subscribe to our Newsletter now!

Related

.png)

Which Lender is Right for Your Business in 2025? Banks, Money Lenders, or Alternative Finance

Jul 02, 2025